In July 2026, a Danville investment firm called 300 Venture Group paid $10.7 million for 8.4 acres at Stoneridge Shopping Center in Pleasanton, California. The land included the shuttered Nordstrom building and, more to the point for the buyer, the surface parking lot wrapped around it. Founder Kameron Klotz called it a “large-scale, infill redevelopment opportunity in a supply-constrained market.” Nobody bought that parcel to sell shoes. They bought it for the asphalt.

That deal is one small, specific instance of a much bigger shift moving through American retail real estate. The parking lot has stopped being a fixed cost of doing business and started being the most valuable line item on the site.

For decades, retail parking was set less by actual demand than by municipal minimums, arbitrary formulas in zoning code that told developers how many spaces to build regardless of whether shoppers ever filled them. Those formulas assumed one behavior: everyone drives, every trip, every time. That assumption is being unwound from two directions at once, and grocery and retail anchored parcels sit squarely in the middle of it.

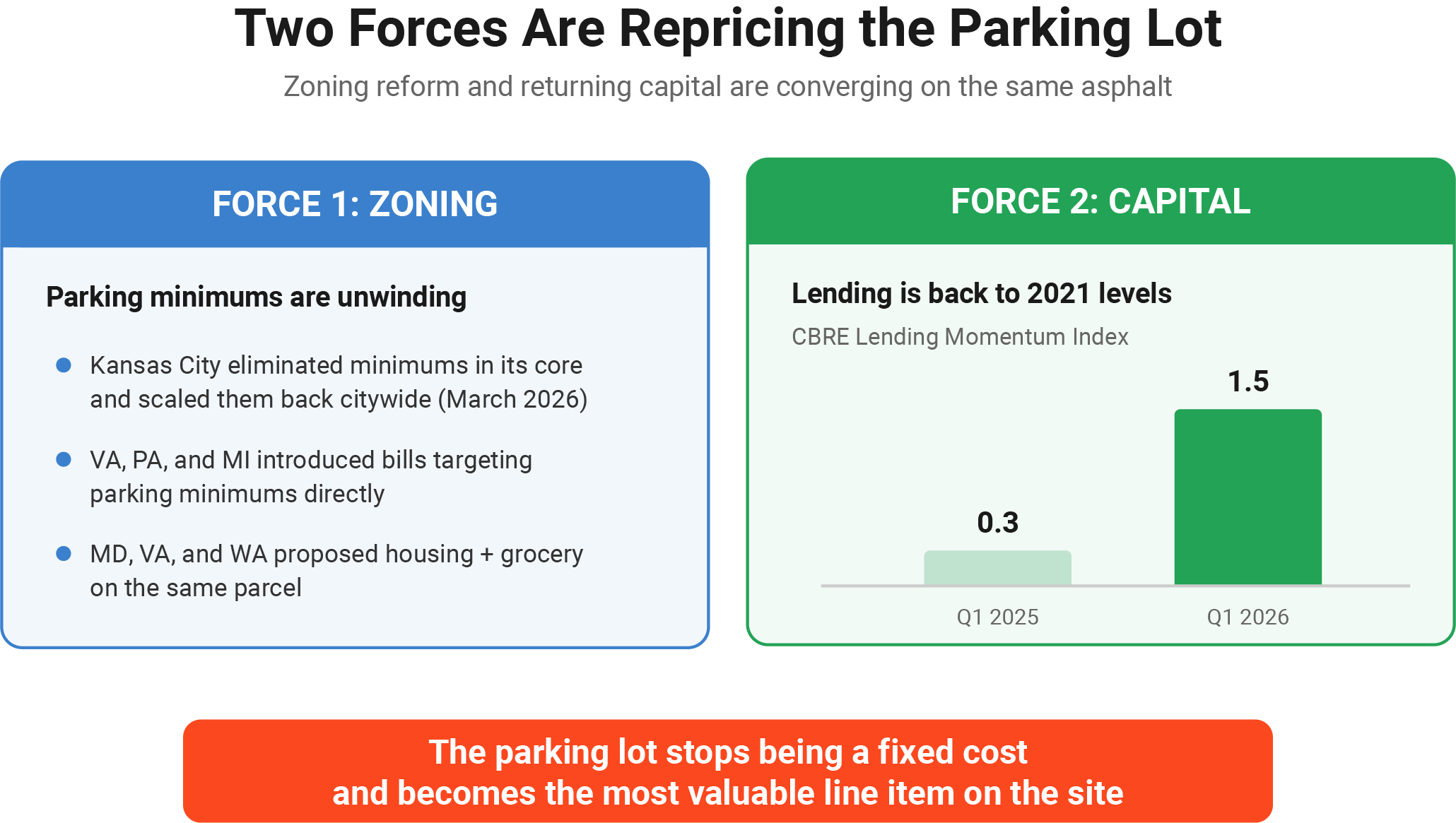

The first direction is zoning. Kansas City voted to eliminate parking minimums in its core and scale them back citywide in March 2026, part of a broader development code overhaul. A local transportation advocacy group framed it simply: older buildings can now be reused without unrealistic parking requirements. Kansas City is not alone. Smart Growth America's March 2026 roundup found states moving on parking reform from both sides. Virginia, Pennsylvania, and Michigan all introduced bills targeting parking minimums directly. Maryland, Virginia, and Washington went further, proposing rules that let housing and grocery stores share the same parcel, parking requirements and all.

The second direction is capital. Commercial real estate lending activity climbed to its highest level since 2021 in the first quarter of 2026, according to CBRE's Lending Momentum Index, which rose to 1.5 from just 0.3 a year earlier. That matters because unlocking a parking lot's value requires financing whatever gets built in its place: apartments, a food hall, a hotel, and for the first time in a few years, that financing is easier to get.

Put those two forces together and you get projects like Shopoff Realty Investments' Bolsa Pacific, an 83 acre redevelopment of the former Westminster Mall in Orange County that broke ground this year. The plan folds a Target anchored 210,000 square foot retail component into 2,250 apartments and homes, a 15,000 square foot food hall, a 120 room hotel, and 15 acres of open space, all on land that used to be a mall parking field. In Florida, Related Ross, began leasing Village Landing, a 71 acre project in Wellington with more than 320,000 square feet of retail and restaurant space alongside office, hotel, and condo product. Back at Stoneridge, 300 Venture Group is weighing “retail re-use and mixed-use densification” on the Nordstrom parcel, the same playbook it ran when it bought the mall's old JCPenney building in 2022.

The catch is that this only works when the capital stack and the housing market cooperate, and right now that is not universal. In Canada, the same thesis is running into a wall. Dixie Outlet Mall in Mississauga entered receivership in March 2026 after its owners failed to service more than $156 million in debt, one of several Canadian malls, including Toronto's Woodbine Centre and Edmonton City Centre, where redevelopment plans stalled as condo presales collapsed and construction costs climbed. Retail analyst Antony Karabus, quoted in Retail Insider, put the mechanism plainly: “In many cases, the parking lot became more valuable than the mall itself. But that only works if you can actually build the alternate use and create the communities. Right now, that assumption is being challenged.” Same math, different market conditions, opposite outcome.

For grocery anchored centers specifically, the stakes look a little different. Grocery stores already sit on some of the largest parking fields per square foot of any retail use, sized for holiday peaks that happen a few weeks a year rather than an average Tuesday. The bills bundling housing with grocery in Maryland, Virginia, and Washington are a signal that regulators are starting to treat that oversized footprint the same way investors are treating dead department store lots: as underused land waiting for a better plan.

None of this makes the decision easy for the owner standing on the actual asphalt. Whatever gets built next has to answer to zoning entitlements shifting under it in real time, a lender who wants to see the numbers before minimums disappear on paper, and a remaining retail tenant base that still needs some number of spaces near the door even after the mixed-use towers go up. Site feasibility tools like TestFit's Parking Solver exist for exactly that overlap, modeling how much of a given lot can realistically convert once zoning, access, and retained retail parking demand are stacked against each other, before anyone commits capital to a plan that does not fit the site. The Stoneridge parcel will get an answer to that question eventually. So will every other half empty parking lot sitting on land that is suddenly worth more than the store it was built to serve.

.gif)

If you're sitting on a similar parcel and running these numbers yourself, we'd like to hear how the math is shaking out. Feel free to contact us here.